When a fire tears through a kitchen or a pipe bursts behind a bathroom wall, the structural damage gets most of the attention — but the contents of the home tell a different story. Furniture soaked through, electronics coated in soot, irreplaceable documents soaking in standing water.

To manage this complex process, a Packout Estimate is created. This is a detailed, line-item cost document built in industry-standard estimating software that outlines the full projected cost of protecting a policyholder’s personal property after a covered loss. It captures every single phase of the recovery mission, from inventorying, packout, transportation, cleaning and restoring, storage, to the packback.

Unlike standard restoration paperwork, this estimate is first submitted directly to our corporate office for an internal review and approval process to ensure absolute accuracy. Once perfected, it is sent over to the insurance carrier for final approval.

This guide breaks down exactly what a content packout estimate is, how it sets the standard for precision, what line items are included, and why it serves as an indispensable tool for both homeowners and insurance adjusters.

What is a Packout Estimate?

At its core, a packout estimate is the official financial blueprint and inventory ledger of your belongings after they have been safely removed from a damaged property. When disaster strikes a home, structural repairs cannot happen efficiently while furniture, clothes, and electronics are in the way. A contents restoration team must carefully pack, catalog, transport, and store those items in a secure warehouse.

A packout estimate is not the same as a structural or dwelling estimate. While a structural estimate covers rebuilding walls, flooring, and roofing, a packout estimate is scoped exclusively to the contents portion of the claim — the policyholder’s personal property. On most standard homeowners policies, that coverage sits in its own pocket, separate from the dwelling and loss of use coverages.

Why Packout Estimates Matter for Insurance Claims

Contents losses are frequently one of the largest — and most complicated — components of a property insurance claim. Smoke, soot, water intrusion, and microbial growth don’t just damage structures; they infiltrate furniture, electronics, clothing, documents, kitchenware and appliances, and irreplaceable personal items. Addressing that damage without a documented scope and cost framework leads to disputes, claim delays, and overpayments or underpayments that are difficult to untangle after the fact.

According to the National Association of Insurance Commissioners (NAIC), incomplete documentation and unclear contents handling are among the most common causes of claim delays following property losses. A thorough packout estimate directly addresses that risk.

What’s Included in a Packout Estimate

Packout estimates are not one-size-fits-all. The scope — and therefore the cost — varies significantly based on the size of the home or business, the type of loss, the number of affected rooms, and the specific contents involved. That said, most professional packout estimates share a common set of line-item services.

Packout Labor and Transportation Logistics

Getting items out of a compromised structure safely requires skilled labor and heavy equipment. The initial phase includes:

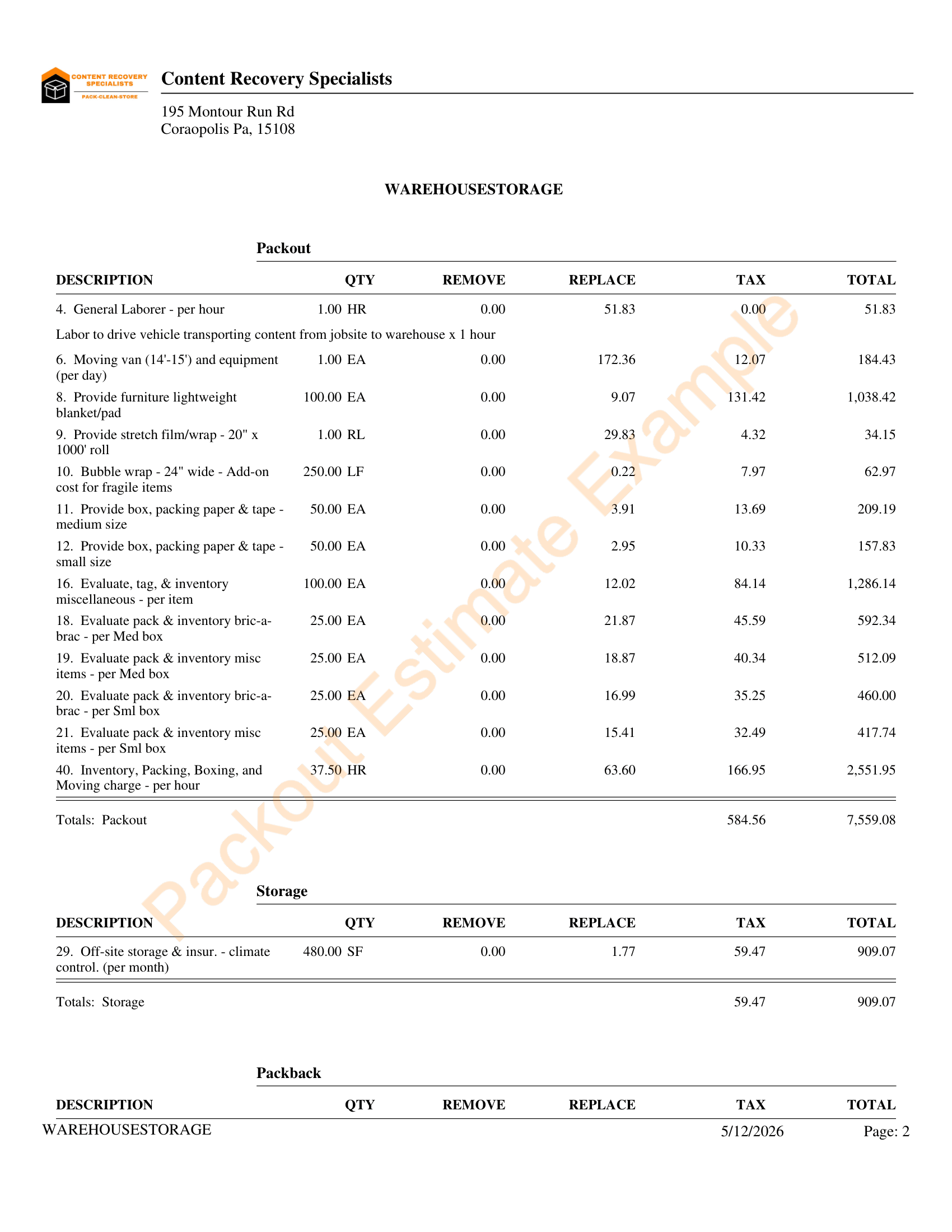

- Inventory, Packing, Boxing, and Moving Charges: The core labor force. This covers the per-hour manual labor required to carefully wrap, box, and load items room by room.

- General Laborer: Dedicated labor hours to drive vehicles, transport contents, and manage the physical transition from the loss location to the secure warehouse.

- Moving Van & Equipment: Daily rental and operational costs for standard fleet moving vans (typically 14′-15′) and associated moving machinery.

Professional-Grade Protective Materials

A significant portion of the estimate covers specialized materials required to shield items from secondary damage during transit and long-term storage:

- Boxes, Packing Paper & Tape (Sized Small & Medium): Granular tracking of boxes utilized, including the structural paper and industrial adhesive tape required to secure them.

- Lightweight Furniture Blankets & Pads: Heavy-duty pads placed between furniture pieces to prevent scratches and structural rubbing during transit.

- Stretch Film / Wrap: High-gauge plastic film rolls used to bind loose items, secure protective blankets around upholstery, and stabilize large structural pieces.

- Bubble Wrap Add-on: Linear footage of shock-absorbing bubble wrap applied explicitly as an add-on cost to safeguard delicate or fragile items.

Evaluation, Tagging, and Detailed Inventory Control

You cannot restore what you do not track. A premier packout requires meticulous chain-of-custody logging:

- Evaluate, Pack & Inventory Bric-a-Brac / Miscellaneous (Per Box): Differentiated sorting fees based on whether a box contains standard non-fragile items or complex, high-detail “bric-a-brac” (such as porcelain figurines, fine china, or intricate collectibles) which demand extended handling times.

- Evaluate, Tag, & Inventory Miscellaneous (Per Item): A digital or physical logging process where miscellaneous items are individually evaluated, barcoded, tagged, and recorded into an inventory system.

Cleaning and Restoration Services

This category is where the restoration expertise of the packout company becomes most visible. Depending on the type and severity of the loss, cleaning and restoration line items may include:

- Content Cleaning — removal of soot, smoke residue, water staining, or biological contaminants from surfaces, upholstery, and hard goods

- Deodorization — ozone treatment, thermal fogging, or other odor neutralization methods for items affected by smoke or mold

- Electronics Restoration — specialized cleaning and evaluation of damaged electronics, which often have salvage value beyond what replacement costs would suggest

- Document and Photo Restoration — freeze-drying and recovery of water-damaged paperwork, records, and photographs

- Textile and Clothing Restoration — laundering, dry cleaning, and odor treatment for fire- and water-affected soft goods

- Furniture Refinishing and Minor Repair — restoration of wood and upholstered furniture where the damage doesn’t warrant total-loss classification

CRS offers a full range of these restoration services across our 40+ locations nationwide.

Climate-Controlled Warehouse Storage

Once packed, items must reside in a controlled environment to mitigate mold, moisture, and temperature-driven degradation. Storage is calculated based on volume and duration The off-site storage & insurance covers monthly square-footage calculations representing the physical footprint dedicated to the policyholder’s contents within a secure, climate-controlled facility.

Packback and Return

The final phase of a packout job is returning items to the property, called the packback. Packback labor, transportation for the return trip, and any unpacking or reinstallation services are estimated as separate line items. This is often scheduled in coordination with the general contractor completing structural repairs, and timing matters — packback too early can expose freshly restored contents to ongoing construction hazards.

Non-Restorable (Total Loss) Documentation

Not every item in a packout can be saved. Non-restorable contents must be carefully documented — photographed, described, and reported — so the adjuster can process a replacement cost or actual cash value payment for those items. CRS generates a formal non-salvageable report for every job, delivered in both PDF and Excel formats with item photos, serial numbers, and model information where available.

How Insurance Adjusters Use Packout Estimates

For insurance adjusters, content claims are notoriously difficult to quantify. Unlike structural damage, which can be measured in linear feet of drywall or squares of roofing, contents involve thousands of individual decisions regarding whether an item can be cleaned (restorable) or must be thrown away (non-restorable).

Adjusters rely heavily on packout estimates for three primary reasons:

- Fraud Mitigation & Chain of Custody: The inclusion of dedicated line items for itemized inventorying provides a digital footprint. Adjusters can review the digital inventory links to verify that items billed for storage match the physical items recovered from the loss site.

- Absolute Auditability: Because the estimate is compiled using finalized quantities of materials used and actual hours worked, adjusters do not have to cross-examine projections. The line items map perfectly to industry-standard estimating platforms like Xactimate.

- Justification of Reserves: The clear division between Packout, Storage, and Packback costs allows adjusters to accurately allocate funds from the policyholder’s Contents Coverage (Coverage C) limits.

Adjusters working with Content Recovery Specialists consistently receive insurance-ready documentation. This documentation chain supports claim closure and reduces the likelihood of disputes after the job is complete.

The Corporate Review: Ensuring Precision Before Submission

A key differentiator in how Content Recovery Specialists interfaces with the insurance community lies in our strict quality control workflow. We recognize that errors in an estimate delay claims processing, causing friction for adjusters and prolonging displacement for homeowners.

To eliminate these roadblocks, each and every content packout estimate is routed to our corporate office for rigorous internal review prior to being sent to insurance adjusters.

Our corporate compliance team reviews the file to ensure:

- Labor hours precisely align with digital time logs recorded on-site.

- Material counts (boxes, bubble wrap, stretch film) correspond exactly to truck manifest records.

- Regional pricing matrices and tax rules match the correct geographic location.

By conducting this internal audit, we ensure that when an estimate lands on an adjuster’s desk, it is flawless, compliant, and ready for immediate approval. For homeowners, this means quicker claim settlements; for adjusters, it translates to a file that can be reviewed and closed with absolute confidence.

FAQ About Packout Estimates

What is a packout estimate used for in an insurance claim?

A packout estimate documents the projected cost of removing, restoring, storing, and returning a policyholder’s personal property after an insured loss. The packout estimate provides adjusters with a line-item breakdown of all labor, materials, and services involved in the packout process, giving both parties a transparent and detailed document.

How long does it take to receive a packout estimate?

Timeline varies based on the size and complexity of the loss. For a standard residential packout, CRS typically prepares and submits an estimate within 24 to 72 hours from when all contents have been packed out. CRS prioritizes fast turnaround because delays in estimate approval can extend the time contents spend in a potentially damaging environment.

Does insurance cover the cost of a packout?

In most cases, yes. Packout services are typically covered under the contents (personal property) portion of a standard homeowners or commercial property insurance policy, provided the loss was caused by a covered peril. Packout costs — including inventory, labor, cleaning, storage, and packback — are charged against the contents coverage limit, not the dwelling limit. Policyholders should review their specific policy and discuss coverage with their adjuster. CRS works directly with insurance carriers and adjusters to submit documentation and facilitate claim approval.

What software does CRS use to write packout estimates?

CRS generates packout estimates using Xactimate, the industry-standard property claims estimating platform developed by Verisk. Xactimate is used by the vast majority of insurance carriers and independent adjusters in North America, which makes CRS estimates immediately compatible with carrier workflows and faster to review and approve. Xactimate pricing is updated monthly based on regional cost data, ensuring estimates reflect current local market conditions.

What’s the difference between a packout estimate and a structural estimate?

A structural (or dwelling) estimate covers the cost of repairing or rebuilding physical structures — walls, flooring, roofing, cabinetry, and so on. A packout estimate covers the cost of managing, cleaning, restoring, and returning the personal property contents of the structure. Both are generated in Xactimate and submitted to the carrier, but they draw from different coverage pockets within the policy: dwelling coverage for structural work and contents coverage for the packout.

Conclusion

Navigating a property damage claim is undeniably stressful for a home and property owner, and managing the moving parts of a complex contents claim can be equally challenging for an insurance adjuster. In the middle of this chaos, a content packout estimate shouldn’t be another source of guesswork or friction.

By delivering a comprehensive packout estimate built on completed work, Content Recovery Specialists replaces administrative headaches with absolute transparency. From the initial boxes packed to the monthly climate-controlled warehouse storage and the final packback home, every dollar is accounted for, fully auditable, and strictly vetted by our corporate compliance team before it ever reaches an adjuster’s desk.

Ultimately, a precise packout estimate does more than just list prices—it ensures a seamless claim process, protects the policyholder’s valuable belongings, and gives both homeowners and adjusters total confidence that the job was done right.